Organic Outpaces the Market: Global Sales Hit Record Highs as U.S. Crosses $76B

As the global food and beverage industry navigates economic headwinds, inflation, and climate volatility, one sector is not just surviving—it is redefining the modern food system. According to a wave of newly released 2026 market reports from around the globe, organic is not slowing down; it is structurally pulling ahead of the conventional marketplace. For business executives, the message is clear: Consumer demand for health, transparency, and sustainability has fundamentally transformed from a niche preference into a primary economic driver.

This article first appeared in Presence Marketing’s April 2026 newsletter.

By Steven Hoffman

In an era defined by fluctuating supply chains and evolving consumer behaviors, the organic food and beverage industry continues to demonstrate remarkable resilience. A trio of recently published annual market research reports from the United States, the European Union, and the United Kingdom reveals a sector that is consistently outperforming the broader conventional food market.

Driven by the mainstreaming of "food as medicine," an increased demand for clean ingredients, and a growing commitment to sustainability, global consumers are speaking with their wallets. Yet, as retail sales rise to unprecedented heights, the industry faces structural and supply-side challenges that require strategic foresight from organic food producers.

The Global Perspective: Record Sales Meet Supply Chain Realities

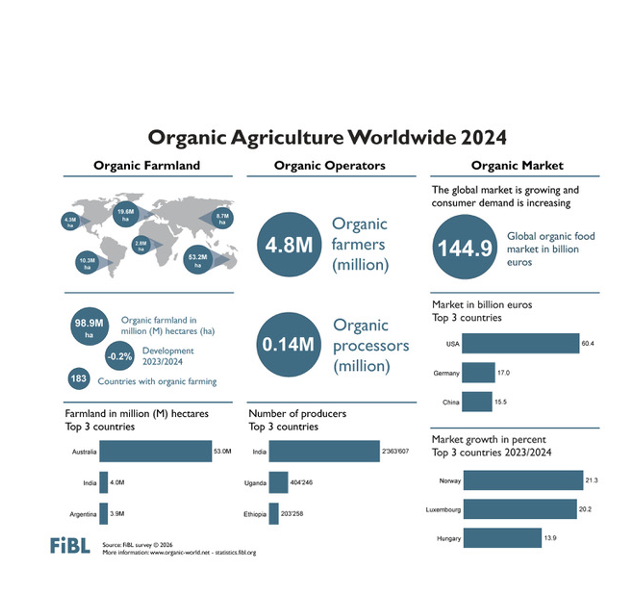

The global organic market has reached yet another milestone. According to The World of Organic Agriculture: Statistics & Emerging Trends 2026, published jointly by the Research Institute of Organic Agriculture (FiBL) and IFOAM Organics International, global retail sales increased 5 percent year over year to nearly 145.0 billion euros ($156.9 billion) in 2024. This represents an all-time high for the sector, pointing to a robust, volume-driven recovery following periods of price-driven inflation.

According to the FiBL and IFOAM data, the global landscape is dominated by a few key powerhouses, though consumption is growing worldwide:

● The United States remains the largest single market for organic food, accounting for 60.4 billion euros ($65.4 billion) in retail sales

● Germany followed as the second-largest global market, generating 17.0 billion euros ($18.4 billion)

● China secured its position as the third-largest market, recording 15.5 billion euros ($16.8 billion) in organic sales

● France represented the fourth-largest market, with sales reaching 12.2 billion euros ($13.2 billion)

When looking at individual consumer habits, Europe remains the epicenter of organic loyalty. Per capita consumption was highest in Switzerland, where consumers spent an average of 481 euros ($521) on organic products in 2024, up from 468 euros the previous year. Denmark followed closely at 373 euros ($404) per person , an increase from 362 euros in 2023. Austria also ranked among the highest, maintaining a steady per capita consumption of 292 euros ($316) year-over-year. Meanwhile, the United States ranked eighth globally, with a per capita organic consumption of 176 euros ($190) in 2024.

However, the FiBL and IFOAM report reveals a dichotomy between soaring consumer demand and agricultural realities. In 2024, almost 98.9 million hectares (244.4 million acres) of agricultural land were organic, including in-conversion areas. This represented 2.1 percent of the world's total agricultural land. Yet, for the first time in years, organic farmland saw a slight contraction, decreasing by 176,000 hectares (434,904 acres), or 0.2 percent compared to the previous year.

This stabilization in acreage is largely attributed to shifting regulatory landscapes—such as the implementation of the new EU Organic Regulation (EU) 2018/848—as well as market disruptions stemming from the energy crisis, rising input costs, and climate variability that delayed farmer conversions. Extreme weather events have heavily impacted key export sectors, specifically commodities like coffee and cocoa. For executives, this signals a critical mandate: securing resilient, long-term supply chains and investing in farmer transition programs will be essential to meeting future demand.

The distribution of organic farmland highlights the global nature of the supply chain:

● Oceania accounted for the majority of organic land, with 53.2 million hectares (131.4 million acres) (Australia accounts for >99 percent of the total organic agricultural land in the entire Oceania region)

● Europe followed with 19.6 million hectares (48.4 million acres)

● Latin America held 10.3 million hectares (25.4 million acres)

● Asia managed 8.7 million hectares (21.5 million acres)

● North America accounted for 4.3 million hectares (10.6 million acres)

● Africa represented 2.8 million hectares (6.9 million acres)

Despite the slight dip in acreage, the human footprint of the organic movement expanded. The global number of organic producers increased to 4,844,872 in 2024. India reported the highest number of organic producers globally, with 2,363,607 farmers. Uganda followed with 404,246 producers. Ethiopia ranked third, registering 203,258 organic producers.

The U.S. Market Surge: Crossing the $76 Billion Mark

In the United States, organic is not just growing; it is redefining the marketplace. According to the 2026 Organic Market Report published by the Organic Trade Association (OTA) on March 4, 2026, U.S. sales of certified organic products reached a record $76.6 billion in 2025.

The data illustrates a sector that is structurally outpacing conventional food. Total U.S. organic sales grew by 6.8% year-over-year, effectively doubling the 3.4 percent growth rate of the overall marketplace. Organic food sales alone hit $70.1 billion, up 6.9 percent and growing three times faster than the overall food market's sluggish 2.3 percent growth.

As has historically been the case, the produce aisle remains the primary gateway for U.S. consumers entering the organic lifestyle. Organic produce accounted for $22.7 billion in sales, representing roughly 30 percent of total organic food sales. Growth within this category was robust, with berries up 10.5 percent, citrus climbing 18.1 percent, and bananas seeing a 12.6 percent boost.

However, the most striking shift in the American diet is occurring in the protein sector. Organic beef has emerged as the fastest-growing segment in the industry, skyrocketing by an astonishing 44.3 percent. This indicates a profound evolution in consumer priorities, where shoppers are increasingly willing to pay a premium for meat products that align with their ethical, environmental and health values. Organic dairy and eggs also saw impressive gains, growing 12.8 percent to reach $9.6 billion.

The concept of "food as medicine" seems to have firmly transitioned from a fringe trend to mainstream consumer behavior. This is most evident in the organic beverage category, which reached $10.2 billion in sales (up 7.2 percent), driven heavily by demand for functional benefits and clean-ingredient profiles. Furthermore, shelf-stable, value-driven organic goods—such as dried beans, fruits, and vegetables—experienced a 13.6 percent surge, proving that shoppers are finding ways to integrate organic staples into their pantries, even amid economic pressures.

As the OTA notes, consumers are consistently choosing trust over price, relying heavily on the USDA Organic seal. If this current trajectory holds, the U.S. organic sector crossing the $100 billion threshold by 2030 is very much within reach.

Import Dependencies: Closing the Supply-Demand Gap

While the U.S. dominates global consumption, its reliance on international trade highlights a critical vulnerability and an opportunity for industry stakeholders. Because domestic organic acreage remains under 1 percent of total U.S. farmland, domestic supply falls significantly short of demand.

The U.S. tracked $5.7 billion in organic imports in 2024. The volume of organic imports into the United States reached 3.25 million metric tons, an increase of 17.7 percent compared to the previous year. Combined, the imports of organic products into the European Union and the United States reached nearly 5.89 million metric tons in 2024.

According to The World of Organic Agriculture 2026 report published by FiBL and IFOAM Organics International, the top exporters supplying these large western markets were Mexico, with 865,076 metric tons; Ecuador, with 765,605 metric tons; and Canada, with 378,820 metric tons. The commodities driving this international trade network highlight consumer reliance on tropical and feed products:

● Bananas were the most imported organic product, totaling 1,365,512 metric tons

● Oilcakes accounted for 593,753 metric tons of total imports

● Sugar represented 535,699 metric tons of the organic imports

The reliance on imported organic feed crops is particularly stark. For instance, U.S. organic soy supply currently meets only about one-third of domestic demand, requiring substantial imports to support the booming organic livestock and poultry sectors.

Complicating this reliance on imports is a rapidly shifting geopolitical landscape. As noted in the FiBL and IFOAM report, earlier U.S. trade policies introduced significant volatility into the supply chain, as President Trump’s tariffs “are having a negative effect on agricultural food imports, more so on the organic sector, as it is heavily dependent on imported raw materials."

The legal and economic reality for organic importers shifted dramatically in early 2026 when the Supreme Court ruled in a 6-3 decision that the International Emergency Economic Powers Act (IEEPA) did not authorize the President to impose sweeping tariffs, effectively striking down the measures, as reported by SCOTUSblog. However, the relief for the organic supply chain was short-lived. Within hours of the ruling, the administration invoked Section 122 of the Trade Act of 1974 to impose a new temporary 10 percent across-the-board global tariff, according to an analysis by the Peterson Institute for International Economics (PIIE).

This rapid pivot means the organic sector continues to face elevated taxes on imported raw materials and feed grains. Furthermore, because these new Section 122 tariffs are temporary—set to expire after 150 days—the environment remains unstable. This forces organic businesses to make critical pricing and supply chain decisions against a backdrop of extreme trade policy volatility.

Complicating matters further is the prospect of potential refunds. Because the Court ruled the IEEPA tariffs were collected illegally, importers may be entitled to recoup billions of dollars in costs. But as Justice Brett Kavanaugh noted in his dissent, the process of refunding these tariffs is likely to be a "mess," leaving organic businesses to navigate complex litigation to recover funds, as highlighted by SCOTUSblog.

Ultimately, because the administration quickly replaced the struck-down tariffs with new ones, overall tariff rates remain similar to their previous levels. Organic businesses continue to face high input costs, which will likely still be passed on to consumers at the grocery store. For C-suite executives, investing in domestic transition programs and expanding local infrastructure is no longer just a marketing win; it is a vital survival strategy for supply chain security in an era of unpredictable trade policy.

The U.K. Perspective: Growth Outpaces Non-Organic

The story of organic resilience extends across the Atlantic. According to the Organic Market Report 2026 published by the Soil Association, and reported by Wicked Leeks on March 19, 2026, 83 percent of U.K. households now purchase organic products.

Despite enduring a severe cost-of-living crisis and rampant food inflation, the U.K. organic market's growth has successfully outpaced the non-organic sector. This trend underscores a broader European and global realization: organic is no longer viewed as an expendable luxury by the majority of consumers. Instead, it is increasingly seen as a non-negotiable investment in personal health, animal welfare and environmental stewardship.

Strategic Takeaways

The convergence of data from FiBL, IFOAM, the OTA, and the Soil Association paints a picture of an industry at an inflection point. Organic is no longer simply growing; it is actively restructuring the modern food system. For business leaders in the natural and organic space, several key directives emerge from these 2026 reports:

1. Capitalize on the Protein and Beverage Boom: While produce remains the foundation of organic retail, the aggressive 44.3 percent growth in U.S. organic beef and the $10.2 billion beverage market point to the next major battlegrounds. Innovating in the functional beverage space and expanding organic protein offerings will be critical for capturing premium consumer dollars.

2. Invest in Supply Chain Resilience: The slight 0.2 percent global decrease in organic farmland paired with record-breaking consumer demand is a recipe for future supply shortages. Brands must proactively partner with growers, offer transition incentives, and secure long-term contracts, particularly for high-risk commodities including coffee, cocoa and feed grains.

3. Lean into Transparency: With consumers navigating a crowded landscape of sustainability claims, the rigorous, third-party verification of the USDA Organic and equivalent international seals remains the gold standard. Brands that clearly communicate the holistic benefits of organic—from soil health to clean ingredients—will continue to win on consumer trust.

As the data makes clear, the global organic market has transitioned from an alternative niche to a dominant force. Executives who align their sourcing, product development, and marketing strategies with this reality will be best positioned to lead the industry as it marches toward the $100 billion milestone and beyond.

Steven Hoffman is Managing Director of Compass Natural Marketing, a strategic communications and brand development agency serving the natural and organic products industry. Learn more at www.compassnatural.com.