Organic Industry Leaders Speak Out in Support of OTA’s Lawsuit Against USDA

Photo by Wikimedia Commons

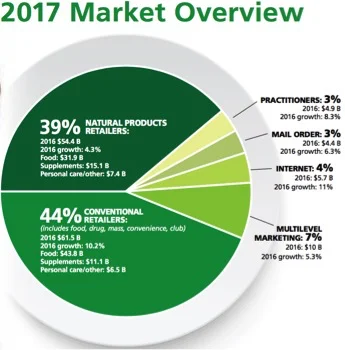

Source: Presence Marketing News, November 2017

Author: Steven Hoffman, Compass Natural Marketing

On January 19, 2017, one day before President Donald Trump’s inauguration, organic industry and animal welfare advocates hailed the release by the U.S. Department of Agriculture (USDA) new Organic Livestock and Poultry Practices (OLPP) rules – the result of a 14-year-long process that would require organic farms to follow improved animal welfare practices. The rule addressed four areas of organic livestock and poultry production, including requiring humane living conditions, animal healthcare, transport and slaughter.

The next day, however, on January 20, the new administration ordered a freeze on all new or pending federal regulations, and delayed implementation of the OLPP rules under the National Organic Program (NOP). In May, USDA asked for additional public input on whether it should enact the rule, suspend it, delay it, or withdraw it. During this new 30-day comment period, USDA received more than 47,000 comments, 99% of which were in support of implementing the new rules by November 14, 2017.

After hearing nothing from USDA since then, on September 13, the Organic Trade Association (OTA) filed a lawsuit against USDA saying it has a duty to protect and advance the U.S. organic sector, and that USDA is in violation of The Organic Food Products Act and the Administrative Procedure Act for its delay of the Organic Livestock Rule. OTA is asking the District Court for the District of Columbia to reverse USDA’s decision to delay and eliminate options proposed to further delay, rewrite or permanently shelve the rule—thereby making the final livestock rule effective immediately, as written.

“In a 60-day period in Spring 2017, the USDA received more than 45,000 positive public comments from farmers, consumers and food producers, agreeing with proposed rules to improve animal welfare, particularly increased pasture access for poultry. Its customers—the public—have spoken, but unfortunately, it seems, they have not been heard,” wrote Matthew Dillon, Clif Bar’s Director of Agricultural Policy and Programs, on September 26 in New Hope Network’s IdeaXchange. “Instead, USDA is listening to a few massive egg producers that want to increase sales into organic markets but not incur the costs of higher animal welfare standards,” he added.

Longtime organic industry leader Gary Hirshberg, Cofounder and Chair of Stonyfield Farm, also spoke out in support of OTA’s lawsuit. “Maintaining the integrity of organic standards, and the consumer trust that we in the organic community work hard every day to earn, demands constant vigilance,” he wrote on October 16 in New Hope’s IdeaXchange. “That’s why the recent legal action by the Organic Trade Association against the federal government over yet another delay in enacting the organic livestock regulations is so critical, and why it deserves the support of all organic stakeholders.”

“The organic industry takes very seriously its contract with the consumer and will not stand aside while the government holds back the meaningful and transparent choice of organic foods that deliver what the consumer wants,” said OTA Executive Director Laura Batcha in a release. “The government’s failure to move ahead with this fully vetted regulation calls into question the entire process by which organic regulations are set—a process that Congress created, the industry has worked within, and consumers trust.”

Natural Products Industry Matures; Independents See Sales Growth

As the natural and organic products industry reached $141 billion in sales on 7.4% growth in 2016, Natural Foods Merchandiser’s 2017 Market Overview reports independents are starting to thrive again as the market shifts.

By Steven Hoffman

Source: Natural Foods Merchandiser, July/August 2017, published by New Hope Network

As a new Managing Editor back in 1986 with the Natural Foods Merchandiser, I was charged with conducting, analyzing and reporting on the natural products industry’s annual retail market overview survey. I recall spending late evenings poring over data with New Hope Network founder Doug Greene to determine overall sales, growth categories and emerging trends. That was when the industry was just breaking $5 billion in sales – a fraction of what it is today.

Thirty years later, the natural and organic products industry is maturing, reaching $141 billion in sales on growth of 7.4% in 2016, according to the 2017 Market Overview, published in the July/August 2017 edition of Natural Foods Merchandiser (NFM) in partnership with Nutrition Business Journal, with additional data provided by SPINS and the Organic Trade Association’s annual organic industry survey.

Over this time, the natural, organic and better-for-you products sector has become widely recognized as a hotbed of innovation and growth in the overall food industry. Point in fact, the Amazon – Whole Foods Market deal announced in June promises to be a game changer not just for the natural products landscape, but also for the entire retail food market worldwide.

Independents Find Stronger Footing

Yet, as the market shifts, independents that have been able to weather the past few years may now find themselves in a stronger position, according to NFM’s 2017 Market Overview.

While sales growth was modest among independent natural products retailers – sales grew 4.3% to $54.4 billion, or 39% of overall natural products sales in 2016 – NFM also reported that 69% of natural products stores surveyed recorded a sales increase, and 72% noted they did not have a competitor open up in their neighborhood in the last year.

“It may go against conventional wisdom, but well-managed and strongly positioned independent grocers can coexist with big retail. While large, often publicly held chains may have scale and strong financial backing, independent grocers are often more agile, enabling them to move quickly to address emerging trends and shifting consumer preferences,” the editors of Food Dive observed in a July 19, 2017, report.

“The difference between the corporate model, which you would now have to say includes Whole Foods, and the authentic, community-owned independent, is becoming clearer every day,” retail specialist Jay Jacobowitz of Retail Insights told NFM. “Those who embrace that authenticity and are passionate about serving their unique community will do well.”

Jacobowitz also noted that while the natural products industry may be maturing, there are areas of the country, including the East South Central region (Missouri, Alabama, Tennessee and Kentucky), that are far from saturated. “It’s a big country, and the big boys can’t be everywhere at once,” Jacobowitz said. “There are still opportunities out there.”

Independents also are more nimble in that they can feature local products, and are often the first to take advantage of such emerging product trends as cannabidiol, or CBD, a new category driving growth in dietary supplements and personal care.

Conventional Retailers Own 44% of Natural Products Market Share

During this time, razor-thin margins, increased competition and price wars impacted large mainstream grocery chains, as well as of some of the “supernaturals.” Kroger reported its first decrease in same store sales in 13 years in March 2017, NFM reported, and Whole Foods Market struggled with declining same store sales throughout 2016, prompting shareholder activism in April 2017 from Jana Partners, which held an 8.8% stake in Whole Foods, and ultimately, the announced sale to Amazon in June 2017.

Other publicly traded supernatural chains, including Natural Grocers and Sprouts, saw their stocks decline in 2016 as a result of increased competition from all sides. Natural Grocers’ stock price continues to be depressed in 2017, though Sprouts’ stock price has rebounded.

Yet, through all that jockeying for market share, the bottom line is that conventional retailers, including food, drug, mass, convenience and club stores, now command the majority of natural and organic products sales.

According to NFM’s survey, in 2016 conventional retailers captured 44% – or $61.5 billion – of all natural and organic products sales, while traditional independent natural products retailers and chains claimed 39% ($54.4 billion) of overall natural and organic products sales in 2016. Additionally, while sales among independents grew a modest 4.3%, sales of natural and organic products among conventional retailers grew at double digits, or 10.2%, in 2016.

Here Comes the Internet

As consumers become ever more comfortable shopping on the Internet from the comfort of their homes, offices and mobile devices, ecommerce sales of natural and organic products grew 11% to $5.7 billion in 2016, capturing 4% of overall natural products sales, reported NFM’s Market Overview survey.

Online sales are sure to continue a strong growth curve, as ecommerce retailers such as Thrive Market, meal kit providers including GreenChef.com and independent brick and mortar retailers increase their online presence. Plus, a growing number of manufacturers are finding markets by creating their own online shopping pages and also by offering their products on Amazon, which continues its juggernaut as the dominant force in online retail. (With its acquisition of Whole Foods Market, it will be exciting to see how Amazon integrates and advances its brick and mortar and online retail strategies.)

The online channel is likely to capture significantly more market share in the next decade from brick and mortar stores, predicted a January 2017 report by Food Marketing Institute and Nielsen. Online sales could grow five-fold over the next 10 years, with U.S. consumers spending $100 billion on “food-at-home” items by 2025, FMI and Nielsen predicted. The report also found millennial shoppers surveyed were more willing to buy groceries online in the future than other consumer groups.

Health supplements, in particular, are benefitting from ecommerce, with $2.6 billion in online sales reported in 2016 by market research firm 1010Data. Brands that focus on “natural” products experienced the most online sales growth last year, 1010Data reported.

Herbal Blends, CBD Drive Supplement Sales Growth

Sales of herbal and homeopathic products increased 13.4% over the 52 weeks ending March 19, 2017, to reach a market value of nearly $2 billion, according to SPINS data shared in NFM’s Market Overview. Vitamin and supplement sales also grew 3.5% to approximately $12 billion in sales. Overall, SPINS reported 5% growth, valuing the total supplements market at approximately $14 billion.

SPINS also reported that sales of herbal blends grew 22% over the previous year, accounting for much of the herbal category’s success. According to research firm Mintel, consumers are responding to supplement formulas that call out benefits, rather than ingredients—and blends often meet that criteria, NFM reported.

Other top-performing supplements in 2016 include turmeric/curcumin and cannabidiol, or CBD, which is emerging as a leading supplement for anxiety and pain management. Despite the regulatory grey area surrounding CBD, sales of CBD supplements grew more than 1700% last year, primarily in the natural channel, reported Hemp Business Journal. Leading market research firm SPINS named CBD oil one of the “ingredients to watch” in its 2016 Trend Watch report.

Other supplement categories of note include organic supplements, which grew 7.4% in 2016. Retailers in NFM’s Market Overview survey also cited probiotics, bone broth and kombucha as top growth categories.

Other categories showing strong growth in 2016 include organic meat, fish and poultry (9.1% growth); organic beverages (6%); organic condiments (6.3%); and organic personal care and other products (8.1% growth in 2016).

The Indie Universe: Over 26,000 Independent Stores

Among NFM’s findings is that, among independent natural products retailers, on average, 60% of a store’s offerings are organic and 40% are described as “natural.” Also, roughly half of all sales in independent natural retail stores are from products that are “Non-GMO certified.”

Additionally, NFM estimates there are 26,042 independent stores in the U.S., including health food stores, natural foods stores and supermarkets, specialty food stores, personal care and herb shops and related boutiques and kiosks, and natural chains including Whole Foods Market, GNC, Vitamin Shoppe, Natural Grocers by Vitamin Cottage, Sprouts Farmers Market, PCC, Earth Fare, Fresh Thyme Farmers Market, MOMs Organic Market, and others.

Click here to download the complete 2017 Market Overview report, including all data charts, published in the July/August 2017 edition of Natural Foods Merchandiser.

# # #

Steven Hoffman is Managing Director of Compass Natural, a full service agency dedicated to Public Relations, brand marketing, digital communications, social media, and strategic business development in the healthy lifestyles market for natural, organic, regenerative and eco-friendly products and services. Contact steve@compassnatural.com.

Regenerative Agriculture a Low-Cost Solution to Climate Change

Regeneration International, a nonprofit organization dedicated to advancing organic, regenerative agriculture, a solution to combat climate change.

Source: Wikimedia Commons

Editor's Note: Compass Natural's Director Steven Hoffman will be attending the COP21 Global Climate Summit in Paris in December 2015 on behalf of Regeneration International to promote the power of organic, regenerative agriculture to help feed the world AND cool the planet. Learn more here and on Facebook. What is the cost of preventing global warming? Not that expensive, really, if one considers switching to widely available and inexpensive organic farming practices, reported Rodale Institute in a landmark White Paper published in May 2014.

In fact, said Rodale after conducting more than 30 years of ongoing field research, organic farming practices and improved land management can move agriculture from one of today’s primary sources of global warming and carbon pollution to a potential carbon sink powerful enough to sequester 100% of the world’s current annual CO2 emissions.

Thus, a term coined years ago by organic pioneer Robert Rodale is now newly emerging: Regenerative Agriculture, with the power to "feed the world and cool the planet," say the founders of Regeneration International, a nonprofit organization dedicated to advancing organic, regenerative agriculture and land management worldwide as a solution to combat climate change. Rodale’s researchers point to organic farming as a way to reduce energy inputs and minimize agriculture’s impact on global warming, draw down carbon from the atmosphere into healthy, organic soils, and also help farmers better adapt to rising global temperatures and extreme weather.

“Simply put, recent data from farming systems and pasture trials around the globe show that we could sequester more than 100% of current annual CO2 emissions with a switch to widely available and inexpensive organic management practices, which we term ‘regenerative organic agriculture.’ These practices work to maximize carbon fixation while minimizing the loss of that carbon once returned to the soil, reversing the greenhouse effect, said the study’s authors.

Or, as the Wall Street Journal reported in a May 2014 feature article, “Organic practices could counteract the world’s yearly carbon dioxide output while producing the same amount of food as conventional farming…”

It seems like a powerful solution to climate change lies literally right under our feet.

Conventional Agriculture Adds Heat The global food system is estimated to account for one-third or more of the world’s total greenhouse gas emissions, says Anna Lappe, author of Diet for a Hot Planet. Much of the fossil fuel used in commercial agriculture comes not only from running tractors and machinery, but also because petroleum is a primary ingredient in synthetic pesticides, herbicides and fertilizers, widely used in conventional agriculture.

While insisting that pesticides and GMOs are the only way to feed a growing population, conventional agriculture and livestock production are today a significant part of the problem, says Rodale, and also are responsible for widespread clearing of forests, grasslands and prairies. Palm oil production alone, with its destruction of the world’s largest rainforest region, is why Indonesia is the world’s third largest greenhouse gas producer.

Also, synthetic nitrogen fertilizer is known to release large amounts of nitrous oxide into the atmosphere, a potent GHG and a primary threat to earth’s ozone layer. Synthetic nitrogen fertilizer also is responsible for the Dead Zone in the Gulf of Mexico, an oxygen-depleted area the size of New Jersey in which no fish can survive.

Organic A Cool Solution According to Dr. David Pimentel of Cornell University, author of Food, Energy and Society, organic agriculture has been shown to reduce energy inputs by 30%. Organic farming also conserves more water in the soil and reduces erosion. Also, healthy organic soils tie up - or sequester - carbon in the soil, helping to reduce CO2 levels in the atmosphere.

“On-farm soil carbon sequestration can potentially sequester all of our current annual global greenhouse gas emissions of roughly 52 gigatonnes of carbon dioxide equivalent (~52 GtCO2e). Indeed, if sequestration rates attained by exemplar cases were achieved on crop and pastureland across the globe, regenerative agriculture could sequester more than our current annual carbon dioxide (CO2) emissions,” Rodale concluded.

Farming in a Warmer Future Changes in temperature caused by global warming could have dramatic effects on agriculture. Extreme weather, rising temperatures, drought and flood caused by global warming all could have an adverse impact on yield, disease and insect pests.

Organic farmers may be better able to adapt to climate change, in that healthy organic soils retain moisture better during drought, making it more available to plant roots. Also, organic soils percolate water better during floods, helping to decrease runoff and soil erosion.

According to Rodale Institute’s 30-year field trials, in good weather, yields for organic and conventional corn and soybeans are comparable. However, organic soils are 28-70% higher in production in periods of drought compared to conventional soils. Researchers at the University of Michigan similarly found that while yields are comparable in developed countries, organic farms in developing countries can produce 80% more than conventional farms.

Rodale also found that during flood, there is 25-50% more water infiltration in organic soils, thus preventing runoff and erosion. Carbon-rich organic soils act as a sponge: for every pound of carbon increased in the soil matter, you can add up to 40 lb. of additional water retention, says Rodale.

For developing nations, organic farming could make a huge difference in adapting to climate change. According to the UN Food and Agriculture Organization, organic farming can be more conducive to food security in Africa than most conventional production systems, and it is more likely to be sustainable in the long term. Furthermore, the FAO found that organic agriculture could build up natural resources, strengthen communities, and improve human capacity, “thus improving food security by addressing many different causal factors simultaneously.”

The National Sustainable Agriculture Coalition reported, “Sustainable and organic agricultural systems offer the most resilience for agricultural production in the face of the extreme precipitation, prolonged droughts and increasingly uncertain regional climate regimes expected with rapid global warming.”

Resources:

The Heroes: Companies Supporting GMO Labeling

In Colorado, while multi-billion-dollar, multinational corporate opponents have pumped nearly $17 million into the state to try to defeat Prop. 105.

Source: Pexels

In Colorado, while multi-billion-dollar, multinational corporate opponents have pumped nearly $17 million into the state to try to defeat Prop. 105, the 2014 ballot initiative to label GMO foods, the grassroots Yes on 105 side has raised just under $1 million in campaign funding. The Yes on 105 campaign is using these funds - contributed by hundreds of Colorado residents, and a small group of leading natural and organic products companies and consumer advocacy groups - tohelp educate voters and get out the yes vote via newspaper and digital advertising, an extensive volunteer network, phone banking, and social media - and to endure a withering onslaught of negative, deceptive television advertising and direct mail from the No on 105 side.

Put these brands contributing to consumer transparency and truth in labeling on your shopping list. Support the brands that have stepped up to contribute to Colorado's grassroots Prop. 105 Ballot Initiative to Label GMO Foods against a $17 million onslaught by Monsanto, Pepsi, Coke, Kraft, Dow, Dupont, Hershey, J.M. Smucker, Mead Johnson, Abbot Nutrition, Conagra and others.

Compass Natural Marketing and its principal Steven Hoffman have served as the lead fundraiser and industry communications specialists on behalf of Yes on 105, Right to Know Colorado - GMO. For more information, visit www.righttoknowcolorado.org.

The Heroes: Support these Companies that Contributed to Yes on 105 to Label GMO Foods in Colorado*

More than $200,000 Food Democracy Now! Presence Marketing/Dynamic Presence

$50,000 - $100,000 Annie's Inc. Organic Consumers Fund

$10,000 - $50,000 Boulder Brands Lundberg Family Farms Dr. Bronner's Applegate Farms Clif Bar Nature's Path UNFI Hain Celestial Group Alliance for Sustainable Colorado

$5,000 - $10,000 Amy's Kichen Frontier Natural Products Co-op KeHE Distributors Nutiva Stonyfield Farm

$500 - $5,000 Daiya Foods Food & Water Watch Justin's .Organic Lucky's Market Door to Door Organics Suja Food Babe Living Maxwell New Belgium Brewery Snack Out Loud Red Idea Group Front & Center Marketing Vital Farms Good Earth Natural Grocery Lucky's Market

Special Thanks Natural Grocers by Vitamin Cottage Whole Foods Market Chipotle Mexican Grill

Acknowledgments Alex and Ana Bogusky Steve and Grace Hughes Organic & Non-GMO Report The Crunchy Grocer Alfalfa's Market Compass Natural Marketing Journeys for Conscious Living Durango Natural Foods Co-op Jared Polis John Foraker Joshua Kunau and Jeremy Siefert, GMO OMG Robyn O'Brien Quinn Popcorn Silver Hills Bakery The Organic Dish Meetings and Events Sandy Gooch and Harry Lederman

Visit our Donors Here: http://www.righttoknowcolorado.org/donors Visit our Endorsers Here: http://www.righttoknowcolorado.org/endorsements

Join a growing number of supporters of GMO labeling. To contribute to Right to Know Colorado to Label GMOs, visit www.righttoknowcolorado.org to make an online donation. For corporate or individual contributions, contact Steven Hoffman at steve (at) compassnatural.com.

Please help us win in Colorado, for all Americans.

* Sources: Right to Know Colorado, www.righttoknowcolorado.org Colorado Secretary of State Elections Division, reporting as of Oct. 27, 2014, http://tracer.sos.colorado.gov/PublicSite/SearchPages/CommitteeDetail.aspx?OrgID=25377

Horst Rechelbacher: Game Changer in Cosmetics, 1941 - 2014

Horst Rechelbacher, founder of Aveda and a game changer in the cosmetics world advocating for beauty products that are healthier for people and the planet.

Source: Pexels

This post is dedicated to Horst Rechelbacher, founder of Aveda and a game changer in the cosmetics world advocating for beauty products that are healthier for people and the planet. Horst also founded Intelligent Nutrients, a line of impeccable body care products so organic and clean you could eat them. Horst passed away peacefully at his home in Osceola, WI, on Feb. 15, 2014, at the age of 72. I met Horst in 2007 when I served as Director of The Organic Center, a nonprofit organization dedicated to advancing scientific research and education about the benefits of organic food and farming. Horst was a major benefactor of the Center, and in working together at The Organic Center and subsequently as advocates of GMO labeling, we became friends. In visiting with him and his wife Kiran on numerous occasions in Minneapolis, Wisconsin and elsewhere, I learned more of his business philosophy, his commitment to health and the environment, his approach to product formulations, marketing, style and art, his great love for people and the planet, and his kindness and generosity. He enriched the world as much as he was enriched by what he did for it, and us. Though I only met him later in life, he left a great influence, and his friendship is a gift I will treasure.

In April 2012, we had the great honor of featuring Horst as the keynote speaker of At the Epicenter, a quarterly entrepreneurship speaker series my company produces in partnership with Best Organics Inc., a leading brand promotions and organic gift basket provider based in Boulder. In this 14-minute video segment, conducted in a CEO-armchair style interview with Seleyn DeYarus, CEO of Best Organics, Horst shares his story and his approach to business and life.

Born in Klagenfurt, Austria, Rechelbacher learned about the plant world from his mother, an herbalist. That knowledge became the centerpiece of his career and a passion that grew through the decades. An award winning hair stylist by the age of 14, Horst emigrated to the US in the 1960s, settled in Minneapolis and founded Aveda after formulating shampoos in his kitchen for clients who wanted more natural, earth friendly products. Horst was also a prolific artist, photographer and art collector, and he supported a number of causes related to health, clean cosmetics and the environment. Horst sold Aveda to Estee Lauder for $300 million in 1997, after building it into an international brand. With Intelligent Nutrients, he kept pushing the boundaries of organically produced beauty care.

“He saw himself as an environmentalist, and increasingly more so over time,” Horst's wife, Kiran, told the Minneapolis Star Tribune. “He saw the plight of the planet and the ongoing damage we’re incurring. He felt that very intensely, and saw that the way he could contribute to improving that was thinking about choices people were making from the consumer point of view — their purchasing power.”

Horst was one of the early pioneers in beauty care who knew that it's not just what you put in your body, but also what you put on your body that counts, and that should be non-toxic, healthful products that were produced in an eco-responsible manner. He left a great legacy for the cosmetics industry, and health-conscious and environmentally aware consumers worldwide. Horst Rechelbacher will be greatly missed.

Read Horst's book, Minding Your Business, first published in 2008.

At the Epicenter Presents: The Natural World According to Bill Weiland

At the Epicenter, on February 20 will host Bill Weiland, founder and CEO of Presence Marketing / Dynamic Presence.

Boulder’s premier sustainable business entrepreneurship speaker series, At the Epicenter, on February 20 will host Bill Weiland, founder and CEO of Presence Marketing / Dynamic Presence, the nation's leading independent natural and organic products brokerage. Named by Forbes as a "Top 25 Consumer Products Kingmaker," Bill Weiland will talk trends driving the healthy lifestyles market. At the Epicenter is produced by Compass Natural Marketing and Best Organics Inc. For more than 20 years as President and CEO of Presence Marketing / Dynamic Presence, Bill Weiland has become a leading expert in forecasting and marketing consumer product trends in the natural, organic, and healthy lifestyles arena. At the Epicenter is pleased to host Bill on February 20 in Boulder for an interactive conversation with local and regional business leaders to discuss upcoming trends in the healthy lifestyles market as well as the future of consumer transparency and GMO labeling.

Recently named by Forbes as one of the “Top 25 Most Influential “Kingmakers” in Consumer and Retailer Companies,” Bill Weiland has dedicated his career to promoting natural foods and health. Presence Marketing / Dynamic Presence is the largest independently owned natural and organic products brokerage in the U.S. Weiland and his team work closely with leading retailers, distributors and manufacturers, and he will share insights for how entrepreneurs and innovators can get their natural and organic products on the shelves.

"In working with leading national brands as well as successful startups, Bill has a keen eye on consumer and product trends driving the rapidly growing healthy lifestyles market,” said Steven Hoffman, co-producer of At the Epicenter and Director of Compass Natural Marketing. “We're excited that he will share his expertise with local and regional entrepreneurs. Also, I have had the opportunity to work with Bill on a number of GMO labeling initiatives and can personally attest to his commitment to consumer transparency and truth in labeling.”

At the Epicenter will be held Thursday, Feb, 20, 2014, at the Sterling Rice Group Event Center in downtown Boulder. The evening will begin at 5:30 pm with a welcoming reception including natural and organic beer, wine and appetizers, followed by an interactive conversation with Bill Weiland at 6:30 pm. For press passes or more information contactinfo@compassnaturalmarketing.com.

Tickets are available for adults ($12), nonprofits ($8), students ($6) and a group rate of 3 adult tickets for $30. For tickets, visit www.billweiland-attheepicenter.eventbrite.com.

At the Epicenter Sponsors Gold Sponsors include Sterling Rice Group, Nature’s Path Foods, Boulder Brands (Earth Balance, Glutino, Udi’s Gluten Free and Evol Foods) Silver Sponsors include New Hope Natural Media, Boulder Weekly, Boulderganic, Bonterra and EKS&H Bronze Sponsors include Pax World Investments, Bay State Milling, St. Claire's Organics, EnerHealth Botanicals, Runa and Care2 Supporting Sponsors include Eco-Products Inc., Shine, Boulder Valley Voices, Eldorado Springs Water and Chinook Book

About At the Epicenter

At the Epicenter is a series of interactive talks for entrepreneurs, business and community leaders in the $300-billion market for natural, organic, sustainable and socially responsible products and services. At the Epicenter is produced by Best Organics Inc., a leading organic gift and brand promotions company; and Compass Natural LLC, a leader in LOHAS communications, public relations, strategic marketing, branding and business development.

Launched in 2010, At the Epicenter has featured nationally syndicated radio show e-Town Founders Nick and Helen Forster; B Lab Co-founder Andrew Kassoy; Jenn Vervier, Director of Sustainability at New Belgium Brewery; world renowned author and Founder of Natural Capitalism Solutions, Hunter Lovins; Nature's Path Foods Co-founders Arran and Ratana Stephens; Kim Coupounas Co-founder of GoLite; Bhakti Chai CEO Brook Eddy; Brendan Synnott, Co-founder of Bear Naked Granola; Horst Rechelbacher, Founder of Aveda and Intelligent Nutrients; Bill McKibben, Founder of 350.org; John Elstrott, Chair of Whole Foods Market; local economies expert and author Michael Shuman; Fox Health News correspondent Chris Kilham; author and non-GMO expert Jeffrey Smith; Tom Harding, founding President of the Organic Trade Association; advertising and marketing gurus Alex and Ana Bogusky, noted natural foods retailers Sandy Gooch, Harry Lederman and Cheryl Hughes; and others. Visit www.facebook.com/atheepicenter.

About Best Organics Inc.

Best Organics Inc. is a leading provider of premium, hand-packed, organic and eco-friendly gift basket collections featuring gourmet products from local, regional and U.S.-based producers and leading brands. Its gift collections are presented in beautifully illustrated, reusable gift boxes, and are available at www.AmericasBestOrganics.com, and for corporate gifting. Best Organics Inc. is a Certified B Corporation, a member of the Organic Trade Association, Colorado Proud, and Naturally Boulder, and is a Green America-Approved Business. Contact us or call 303.499.ORGANIC (6742).

About Compass Natural Marketing

Compass Natural, founded in 2002 by healthy lifestyles and LOHAS industry veteran Steven Hoffman, brings more than 25 years of experience in natural and organic products marketing, public relations, social networking, market research, package design, product development, online and print content and design, event planning, business development, and strategic guidance in the $300 billion market for natural, organic and sustainable products and services. Contact info@compassnatural.com, tel 303.807.1042.

The Natural Scene: Will these Food Trends Shape 2014?

Based on my not-so-scientific analysis, here's a look at the some of the trends I'll be following this year.

Source: Pexels

As a former food editor and evaluator of the natural products scene, many times I've wished for a crystal ball to help me determine the next big food product. While there have been plenty of surprises (who could have predicted chia would make its way from infomercial novelty to functional food?) through the years I've landed on a formula for helping me determine what will stick around and what will likely fade away. It seems when innovation meets a market need, a brand is on to something. Sprinkle in quality ingredients at a fair value and success is nearly guaranteed. Based on my not-so-scientific analysis, here's a look at the some of the trends I'll be following this year. Insect protein. Beetles for breakfast anyone? Ten years ago, this idea was total yuck. Fast forward to tomorrow and I won't be surprised if we're sprinkling crushed crickets on our cereal. Think I've missed the mark? Consider that most of the world eats insects in one form or another and the reasons are simple: they're nutritious, sustainable and cheap. I know of at least one innovative company that's experimenting with cricket meal for use in a nutrition bar (think of it like cricket flour). This may be the perfect entry for American consumers who are likely not ready to bight down on bits of antennae or hindlegs in their food snacks—at least, not before noon!

Hyper convenience. On-the-go consumers have long fantasized about the perfect meal in a pill. Pop it, and keep going. While I'll never totally understand this mentality since meal times are built in excuses for taking a break, who's not been hit with hunger pangs and nowhere to turn? Airport terminals, malls, suburbia—these are common danger zones. Convenience foods save the day, and we're learning that the more portable and nutritious a product, the more likely consumers will give it a try… even if it doesn't entirely deliver on flavor. Any early Power Bar fans out there? Manufacturers are experimenting with convenient ways to deliver nutrition that break out from the now boring bar. I've seen fortified ice cream cups, and yogurty push pops, but what's catching my attention is the pouch. Similar to the bar, pouches are great for on-the-go, and can be filled with just about anything. Offerings currently are primarily fruity but I see protein-fortified formulations and possibly even savory options in the horizon.

Pale-eee-ohhhhhh! Blame Crossfit Boxes or simply consider Paleo a rebound from the high-carbohydrate low fat days of our past. Consumers are experimenting with this entirely new style of eating, and I think it will stick around. Why? Much about the Paleo diet is based on sound wisdom. The eating plan emphasizes sustainable meat sources such as buffalo and grass fed beef and encourages consumers to look to whole food sources for daily nutrition.

Big brands appear to be taking a wait-and-see approach before marketing to the Paleo crowd, but smaller companies aren't holding back. Snack formulations emphasize transparency, better-for-you ingredients and minimal sweeteners. Who doesn't like that? Expect more convenient food products such as cereals, cookies and bars made with just nuts, seeds and berries that are Paleo ready even if they're not ready to call out their primal appeal.

Kelsey Blackwell is former Senior Editor of New Hope Natural Media, publisher of Natural Foods Merchandiser and New Hope 360, leading print and online trade publications serving the natural and organic products industry. She is currently based in the San Francisco Bay area.

GreenMoney Journal: GMOs in Our Food: Do We Have a Right to Know?

Test your knowledge on GMOs in food! Compass Natural's Steve Hoffman and Nikki McCord of McCord Consulting co-authored an article in the Fall 2013 edition of GreenMoney Journal: "If you’re anything like us, you’re probably enjoying a snack while checking your email and catching up on your blogs. If you’re eating a conventionally produced snack – that is, one that is not Certified Organic or Non-GMO Verified – chances are it could be full of GMOs. Check your packaging. Did you see the label informing you of this fact? Most likely you didn’t because companies are not required to tell you whether or not GMOs are in your foods. And yet, GMOs are in about 80% of commonly processed foods. So what are GMOs and what is their impact on human and animal health and the environment? . . ."

Who's Driving Growth in Organics?

As sustainable food producers position for the future, they can count on the consumer to drive double-digit sales growth in organic and non-GMO products.

{kind=link}

{kind=link}

Source: Wikimedia Commons

{kind=link}

As sustainable food producers position for the future, they can count on the consumer to drive double-digit sales growth in organic and non-GMO products. In fact, says Wall Street analyst Scott Van Winkle of Boston-based investment bank Cannacord Genuity, the only real growth happening in the food industry today is in the natural, organic and specialty foods markets. Additionally, while California’s Prop 37 GMO labeling initiative was narrowly defeated in November, Van Winkle counters that consumer awareness of genetically engineered foods has increased dramatically as a result of media attention to Prop 37, which will only drive further growth in the natural and organic sector, he says.

However, consumers also became aware during the Prop 37 debate that the parent companies of certain leading organic brands contributed millions to defeat Prop 37, a move that created consumer backlash, exemplified by numerous negative postings on these organic brands' Facebook pages by angry consumers. Companies and brands that support GMO labeling have been lauded as heroes by core consumers.

Shoppers Seek Out Local, Non-GMO Indeed, the Non-GMO Verified Project reports 21% growth in the number of non-GMO verified products in the past year, making it the fastest growing “eco-label” in the U.S., says SPINS.

Buying organic food and products with environmentally friendly packaging makes shoppers feel more positive about their choices, and nearly half (46%) of U.S. shoppers seek out organic and local food, says PricewaterhouseCoopers in its annual report Experience Radar 2013: Lessons from the U.S. Grocery Industry, published in December.

Additionally, shoppers are willing to pay on average a 4% premium for local and organic products, with certain demographics willing to pay premiums of up to 27% for local and organic, and up to 30% on recyclable packaging, says the report.

Financial Markets Respond Seeing the growth in consumer demand for healthy and eco-friendly products, in 2012 the public financial markets opened again after several years to natural and organic products companies, and Cannacord's Healthy Living Index continues to outperform the S&P 500.

In July, Natural Grocers by Vitamin Cottage (NYSE: NGVC), a retail chain founded in the Denver area in the 1950s by health food pioneer Margaret Isely, raised more than $100 million in an initial public offering. Earlier, in March, natural and organic foods brand leader Annie’s Inc. (NASDAQ: BNNY) impressed analysts and industry alike with the biggest opening day gain in stock price in nearly a year. WhiteWave Foods (NASDAQ: WWAV), maker of Horizon and Silk natural and organic products, raised nearly $400 million in a late October IPO. Additionally, popular East Coast gourmet food chain Fairway Market filed in September to raise $150 million.

Organic is creating jobs, too – more than 572,000 U.S. jobs were created in the organic sector in 2010, at a rate 21% higher than the conventional food industry, according to a 2012 Organic Trade Association study. With 9.5% growth in 2011, U.S. sales of organic products totaled $31.5 billion, says OTA, representing 4.2% of overall U.S. food sales.

"Organic lifestyles are not a passing trend. Expect this trend to grow exponentially in the coming years," PricewaterhouseCoopers advised grocers.

Adapted from Compass Natural News, Winter 2013.