Natural Investing: The Movement Toward Natural & Organic Food and Healthy Lifestyles

Originally appeared in the June 2019 edition of GreenMoney Journal.

By Steven Hoffman

Sales of Natural & Organic Products Outpace Conventional Food and Beverage as Consumers Get the Message about the Relationship between Diet and Health

Launching natural and organic products companies, as well as investing in them, is a daunting challenge in today’s shifting and competitive retail and consumer products marketplace. Yet, consumer demand for healthier products continues to grow. With concerns ranging from the cost of healthcare to the effects of food and agriculture on climate change, consumers of all ages are opting for natural, organic and functional foods and beverages, nutritional supplements, natural medicines and other eco-friendly products from mission-based companies, local producers and brands that share their values and address their concerns.

And, with conventionally grown apples included at the top of the Environmental Working Group’s infamous “Dirty Dozen” list of contaminated fruits and vegetables because each conventional apple contains on average 4.4 toxic, synthetic pesticide residues, people are realizing that it’s the organic apple a day that keeps the doctor away. By choosing organic, regenerative and other healthful and eco-friendly products, people are investing most directly in their family’s health, the health of the planet, and the health of family farms and local communities. And it’s translating into sustained business growth in the natural and organic products sector.

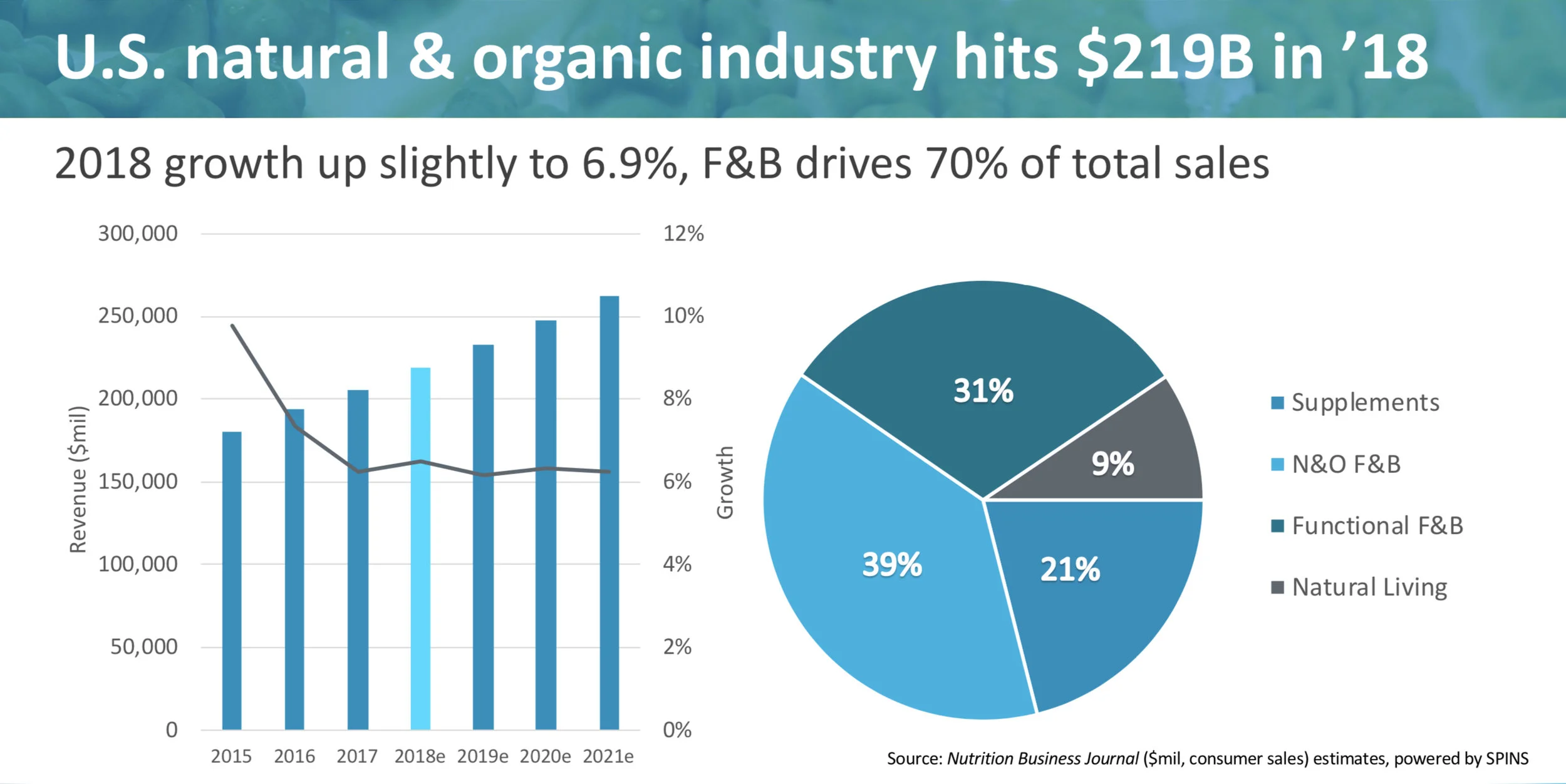

In 2018, sales of natural and organic products increased 6.9% to $219 billion, according industry market research leader New Hope Network, while sales of conventional food and beverage products, totaling $634 billion, declined by -0.2% in the same year. “It’s not news that sales of natural, organic and functional foods and beverages are growing at a far faster pace than conventional food and beverage,” said Carlotta Mast, New Hope’s Senior VP of Content and Insights, in an industry trends seminar presented at Natural Products Expo West in Anaheim, CA, in March 2019. (Attracting nearly 90,000 visitors from over 70 countries, Expo West is the world’s largest natural and organic products trade show.) “The natural and organic products industry is on track to surpass $250 billion in sales by 2021,” Mast added.

In a real sense, Mast noted, conventionally produced, highly processed food and beverage products, made with artificial flavors, colors and other ingredients, are experiencing negative growth. All the growth today in the food and beverage sector is in natural, organic, nutritional, non-GMO and other clean label products. From a small health food and crunchy, hippy movement of independent natural foods stores and co-ops in the 1950s, ‘60s and ‘70s, natural and organic is now leading the way in food and beverage retail and manufacturing innovation – marking a huge shift in the market and in the consumer mindset.

Online vs Brick & Mortar

While manufacturers are compelled in today’s market to pursue what’s referred to as “omnichannel” sales strategies, natural and organic continues to be a “brick and mortar” industry, with 86% of total sales being rung up in either mass market or natural foods stores. Conventional grocery retailers including Kroger, Walmart, Costco and others are taking a larger chunk of the market. According to New Hope data, 60% of total natural and organic product sales are happening in the mass market and mainstream conventional grocery channel, which grew 7.4% to $130 billion in 2018. However, more midsize natural food retail chains such as Sprouts Farmers Market (NASDAQ:SFM), Natural Grocers (NYSE:NGVC) and others, which are dedicated to selling predominately natural and organic products, continue to perform well.

“The natural channel, which helped create this industry and continues to be a vitally important channel, grew at a slower rate of 3.3% to reach about $58 billion in sales in 2018. Although natural is now smaller than the mass market channel, it is still strategically important, particularly for new brands,” Mast said.

Online sales are getting a lot of attention in the natural and organic products space, but according to 2018 data from New Hope Network, e-commerce is driving less than 5% of total sales. However, “that will change pretty quickly over time,” Mast said. E-commerce is becoming increasingly important as a launch pad for new products and brands, and online sales for natural and organic products grew 18% to reach $8.4 billion in 2018. “In a survey of 300 natural brands, half of the new companies that entered the market between 2015 and 2018 started selling online before they moved into any kind of retail distribution. That’s a huge shift for our industry,” Mast noted.

“Even with wild swings in the economy over the past nine years, people are moving into natural for health reasons and not financial ones,” said Nick McCoy, Co-founder and Managing Director of Whipstitch Capital, a leading independent M&A and private placement advisory firm focused on the healthy living consumer market. And the good news for natural products businesses trying to establish themselves in the market is that “retailers are still embracing smaller brands, even in conventional natural food sets. Once people start investing in their health, they’re not likely to go back,” he added.

Categories and Trends Driving Growth in Natural and Organic

Organic: Sales of organic foods and beverages grew 5.6% to become a $45 billion market segment in 2018. According to the Organic Trade Association, the organic industry’s leading trade group, in the last decade alone, the U.S. organic market has more than doubled in size. According to New Hope’s Mast, “Organic is absolutely mainstream now and with increased volume and size has come a slight slowing of growth. Some of this has come from the struggles of organic dairy, which makes up 14% of the category, and last year the organic dairy category continued to see growth plateauing due to oversupply and growing consumer preference for plant-based beverages,” Mast observed. According to New Hope’s data, organic produce – fresh fruits and vegetables – comprises 38% of all organic sales. “Organic supply is lagging behind growing consumer demand, a challenge the organic industry has to address,” Mast added. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM Organics International, leading international organizations based in the EU, the global market for organic food reached an estimated $97 billion US in 2017 (approximately 90 billion euros). The U.S. is the leading market with 40 billion euros, followed by Germany (10 billion euros), France (7.9 billion euros), and China (7.6 billion euros). The Swiss spent the most on organic food (288 Euros per capita in 2017), and Denmark had the highest organic market share (13.3 percent of the total food market). In 2017, 2.9 million organic producers were reported worldwide, a 5% increase over 2016. Total global farmland under organic production increased 20% to nearly 70 million hectares (173 million acres), representing the largest growth ever recorded by FiBL and IFOAM. Yet for all the success of organic, globally, only 1.4% of the total estimated farmland is organic. Organic production, and in particular, Regenerative Agriculture, with its focus on sequestering carbon and building healthy soils, has the potential to help mitigate climate change and is a powerful new movement emerging in sustainable food and farming.

Plant Based: With a $183.8 million IPO filing submitted recently by plant-based meat alternative company Beyond Meat, maker of the Beyond Burger, plant-based foods are now firmly a trend, as more Americans seek “flexitarian” diet options to reduce the consumption of meat and incorporate more plant based options in their diet. According to the Plant Based Foods Association, sales of plant-based foods grew 20% in 2018 to more than $3.3 billion. This growth is significant when compared to the sales of all foods, which grew just 2%, so plant-based foods dollar sales are outpacing dollar sales of all retail foods by 10X, the association claims. In particular, plant-based dairy alternatives are a rapidly growing category with 50% growth reported. This category includes plant-based cheeses, creamers, butter, yogurts, and ice creams (but not plant-based milk). Plant-based milk now represents 15% of the total milk market, says the Plant Based Foods Association.

Hemp and CBD: According to data collected by Nutrition Business Journal, sales of products derived from industrial hemp, including full spectrum hemp extract and CBD products, grew 60% to reach $238 million in 2018. Industrial hemp, while derived from the same Cannabis sativa plant as marijuana, is defined as containing less than 0.3% THC. At such low levels, hemp is the non-intoxicating cousin to marijuana. With more than 25,000 recorded uses throughout human history from building materials, paper and bioplastics to textiles and fashions, superfoods and natural medicines, hemp is rich in other cannabinoid compounds, of which CBD or cannabidiol is the most widely known. These cannabinoid compounds have been shown to be beneficial to human and animal health. In a historic move championed by U.S. Senator Mitch McConnell (R-KY), industrial hemp was legalized in the United States for the first time in over 80 years when the 2018 Farm Bill was signed into law by President Trump in December 2018. For farmers across the country seeking alternative crops to GMO corn and soy and tobacco, hemp has been a godsend. According to industry group Vote Hemp, total acreage under hemp cultivation in the U.S. exceeded 78,000 acres, an increase of nearly 26,000 acres over 2017 estimates. For independent natural products retailers, sales of CBD products, which are now legal across the U.S., though some states and municipalities are still challenging the national law, have also been a boon, enabling them to differentiate themselves from the mainstream retail competition. And while the Food and Drug Administration (FDA) is monitoring sales of CBD products, the agency has indicated it will allow the market to evolve while also keeping a close watch on potential bad players who make misleading or fraudulent claims on products.

Functional Foods and Ingredients: Consumers are opting for food and beverage products that provide real health benefits and functionality, reported Mast, and beverages and functional snacks helped drive 7.5% growth in this category to $68 billion in sales in 2018. The most popular functional ingredients included the herb ashwaganda, pre- and pro-biotics, and hemp and CBD. “The growth in probiotic foods and beverages represent a continued blurring of the lines between dietary supplements and foods and beverages, as consumers have a growing preference for non-pill and non-capsule delivery forms for functional products,” Mast shared. In addition, the “snackification” convenience trend continues to drive expansion in better-for-you and functional snacks.

Dietary Supplements: Sales of nutritional supplements grew 6.1% in 2018 to $46 billion, driven by sales of collagen products, adaptogenic herbs and other botanical products, mushrooms and other immune support products, anti-inflammatory products such as turmeric, pre- and pro-biotics, multivitamins, and CBD and hemp products.

Natural Living: A $20.8-billion category comprising natural personal care and beauty care products, household products and pet care. In addition to pet care, mentioned above, product trends driving this category, which grew 6.5% in 2018, include household cleaners (double-digit growth), organic oral care and feminine care products. Referred to as a “self-care category,” Mast observed that consumers are embracing clean beauty and are paying more attention “not only to what they put into their bodies but also what they put on their bodies and bring into their homes.”

Pet Products: “Natural and organic pet products outperformed all other categories in 2018 – sales growth for the natural pet category was up 10.2% to $7 billion, reported Mast, who also shared that growth in natural and organic pet products far outpaced the 1.9% growth achieved in 2018 by the $26-billion conventional pet products market. “More than 70% of Millennials currently own a pet, according to the American Pet Products Association, and 86% of Millennials believe that natural and better-for-you pet food is vital for the health of their pet,” Mast added.

Sugar Ain’t So Sweet: Other “macro trends” driving the market include changing consumer perceptions around nutrition and healthy fats, and a growing awareness that “sugar isn’t all that sweet when it comes to health.” Diet trends include the Paleo and Keto diets, and convenience still rules, but products have to have great nutrition and taste. Consumers are also becoming increasingly concerned about packaging waste and are looking to support inventive business and ownership models, sustainable sourcing and packaging, and fair trade, socially responsible and mission driven brands.

Where to Invest?

Motley Fool writer Brian Stoffel says, “If you’re looking for the short answer as to who will be the big winners in the organic and natural food movements, the answer is simple: smaller, local organic farmers … and Amazon (NASDAQ:AMZN).” The reasons, he says, include the trend that today’s Millennials – now the largest demographic spending group – want to purchase from brands that are more organic, small, and locally focused. Stoffel posits that when bigger brands buy out smaller natural and organic brands, today’s savvy consumer simply pivots to a different brand that better reflects their desires

On the other side of the coin, Stoffel’s reasoning behind considering online power house Amazon as a major player in natural and organic products is its position as owner of natural products retail pioneer Whole Foods Market, as well as its leadership position in the e-commerce world where it sells millions of natural and organic products at low margins.

In between are a number of publicly traded companies including distribution leader UNFI (NYSE:UNFI) and mid-size natural and organic products retail chains Sprouts Farmers Market (NASDAQ:SFM) and Natural Grocers (NYSE:NGVC). Seeing the shift in consumer preference to natural and organic, major retailers including Kroger (NYSE:KGR), Costco (NASDAQ:COST), Walmart (NYSE:WMT) and others have all become significant sellers of natural and organic products. Kroger, which reported more than $16 billion in natural and organic products sales in 2017 and double-digit growth of natural products over the past several years, also is a majority investor in Lucky’s Market, a rapidly growing, midsize natural and organic products retail chain with 35 stores in 11 states.

In the exploding market for hemp and CBD products, a handful of companies have emerged as market leaders, among them some publicly traded companies including Charlotte’s Web (NASDAQOTH:CWBHF), Elixinol (OTCMKTS:ELLXF), CV Sciences, sold under the brand name +CBD Oil (NASDAQOTH:CVSI), Isodiol International (CNXS:ISOL), Aurora Cannabis (OTCMKTS:ACBFF), Canopy Growth (NYSE:CGC), and others.

As a closing piece of advice, independent natural foods retailer Philip Nabors, co-founder of the family owned Mustard Seed Market in Akron and Cleveland, OH, proffers that while an investment in market giant Amazon might seem attractive, it does not necessarily support local business and economies. “Green investors who want to place some of their funds in higher risk investments might want to consider investing in local businesses, where such investments can more directly impact local communities” – and also where individual investors can invest not only money, but potentially time, energy, resources, and relationships, and be rewarded with a more immediate connection in the communities in which they live, and in the long run as these businesses grow and build value, he says.